S&P500 Trading Update 6/5/26

S&P500 Trading Update 6/5/26

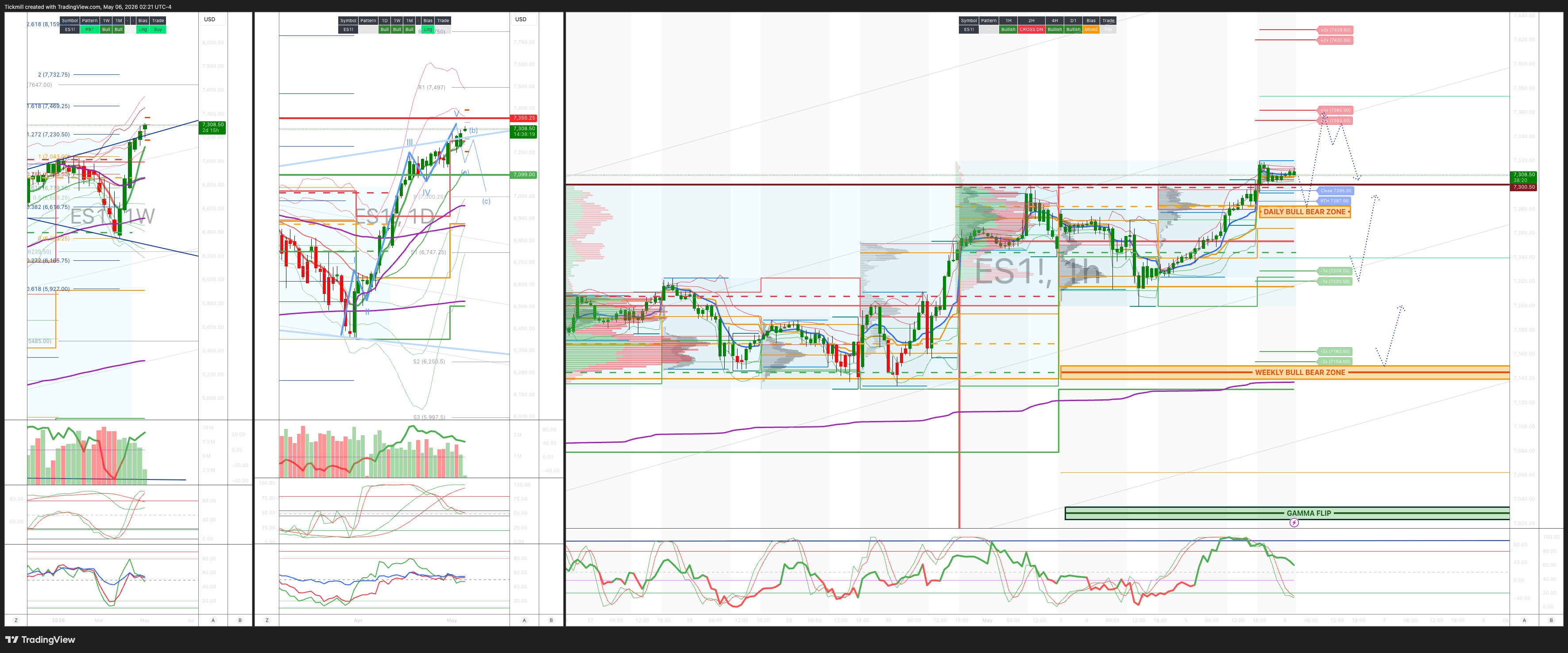

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7150/40

WEEKLY RANGE RES 7356 SUP 7138

May OPEX Straddle: 225pt range implies a OPEX to OPEX range of [6900, 7350]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.16 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7253

WEEKLY VWAP BULLISH 7118

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – OTFH - 7157

WEEKLY STRUCTURE – OTFH - 7137

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7270/80

GAMMA FLIP 7030

DELTA FLIP 6950

DAILY RANGE RES 7353 SUP 7220

2 SIGMA RES 7420 SUP 7154

VIX BULL BEAR ZONE 19.5

TRADES & TARGETS

LONG ON TEST/REJECT DAILY BULL BEAR ZONE TARGET DAILY > WEEKLY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Meltup’

US equities resumed the melt-up, led by a sharp rotation back into semis, memory and broader TMT. S&P +81bps to 7,259, NDX +131bps to 28,015, R2K +175bps to 2,845, and Dow +73bps to 49,298, despite a -$1.5bn MOC sell imbalance. Volumes remained below trend at 16.3bn shares versus a 18.2bn YTD average, but activity improved across TMT. Cross-asset was supportive enough: WTI -364bps to $102.55, 10Y unchanged at 4.42%, VIX -498bps to 17.38, gold +74bps to $4,567, DXY +11bps to 98.48, and Bitcoin +216bps to $81,664. The key difference from Monday was oil relief without another rates backup, which gave equities room to refocus on earnings, AI infrastructure and supply-chain optionality. The catalyst was the overnight report that Apple is weighing Intel and Samsung as potential foundry partners for device processors, creating a second-source narrative beyond TSMC and igniting the chip complex, with INTC, MU and SNDK all up 10%+. The tape is increasingly clear: investors are willing to pay for credible AI infrastructure, memory pricing power, foundry optionality and earnings revisions, while punishing anything that fails the “beat-and-raise with visibility” test.

Flows were more constructive than the prior session, though not universally bullish. The floor was 5/10 in activity and finished +3% to buy versus a 30-day average of +62bps. Long-only activity picked up meaningfully across TMT, suggesting real money is continuing to concentrate dollars into secular growth winners and reacting to recent earnings datapoints. That gives the rally better durability than a purely fast-money squeeze, and keeps dips in high-quality TMT buyable. Still, this is not a blanket “buy everything” tape: asset managers finished roughly $2bn net buyers, but hedge funds sold macro and tech while buying healthcare and communication services. Post-close earnings reinforced the dispersion message. AMD +6% after a beat/guide above and positive commentary, stabilizing AI compute sentiment. SMCI +19% as gross margin upside offset a topline miss. FLEX +7% on a large beat and guide above Street. MTCH +4% guided EBITDA above consensus. LITE +1% beat and guided revenue above Street, though against a high bar. On the negative side, ANET -10% beat the quarter but guided revenue only slightly above Street, which was not enough. KVYO -18% traded lower on a CFO departure and June revenue guidance of only +1% q/q with y/y deceleration. WK -6% guided 2Q revenue below Street despite a slight FY raise, and FRSH -3% showed that even a beat/raise can be faded if expectations are already elevated.

Derivatives told a similarly constructive but selective story. The tech-led rally drove NDX vol outperformance, with NDX vols bid across the curve, especially in the front end, while SPX vols were small bid across tenors. Demand for QQQ vol remained notable even as the QQQ/SPX vol spread widened, suggesting investors are still willing to own convexity around the leadership complex rather than only hedge downside. Skew compressed, reversing Monday’s steepening, as the market shifted from macro-hedging back toward upside and earnings participation. Dealers are long gamma, which has limited front-end convexity on the rally, but the desk still thinks short-dated premium is ownable at these levels. Hedges out to end-May or the first week of June remain popular because they capture NVDA earnings, AVGO earnings, NFP and geopolitical/oil headline risk. The straddle through the end of the week went out at 95bps.

Trading takeaway: stay constructive, but be precise. The tape can keep working higher if oil cools and rates remain stable, but the leadership is narrow and the earnings bar is high. Prefer high-quality TMT, memory, semis and AI infrastructure names with clean revision stories, but avoid blindly chasing 10%+ moves without defined risk. AMD’s print should help stabilize semi sentiment, while Apple’s potential foundry diversification keeps the INTC/Samsung/supply-chain optionality theme alive. At the same time, use skew compression on rallies to rebuild downside protection, because the oil/Iran shock has paused rather than disappeared. Best expressions are semi/memory momentum via call spreads, long quality TMT versus short expensive growth misses, and end-May/early-June option structures that capture NVDA, AVGO, NFP and geopolitical risk. Bottom line: this remains a buy-the-dip market when oil and rates behave, but it is a dispersion tape, not a broad beta tape.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!